Cell phones are part of us now. Most of our lives are spent inside inches of a cellular gadget. We’d like them nearly like we’d like meals and water. They permit us to run many of the logistics of our life wherever we could also be. They permit us to consistently talk — merging life and work right into a seamless material. For good or dangerous, our lives at the moment are much less compartmentalized and extra built-in right into a unified circulate of knowledge, work, wellness, communication, buying, leisure, and maintenance.

Nonetheless, telephones and cellular providers are dearer than ever. This has positioned cell phone service suppliers beneath elevated buyer worth scrutiny, particularly as a result of there are so few suppliers and so many subscribers. The sheer quantity — the ratio of subscribers to suppliers — is staggering. It has stretched cellular supplier billing programs and it has annoyed tens of millions of shoppers. It has additionally made competitors fierce.

Take into consideration your personal cellular supplier expertise, particularly about billing and repair. Because the huge three (AT&T, Verizon, and T-Cell) largely carry the identical telephones, they’re now in a scenario the place worth, service and billing are presumably the best determiners of buyer loyalty and retention. What drives you to remain or swap? Are you all about value or do you prioritize utilizing a customer-friendly model that makes cellular use a rewarding expertise and gives different worth?

Buyer loyalty is fragile in any business; insurance coverage is not any exception.

Nice buyer experiences, interfaces, straightforward transactions, and intuitive service can construct your model and improve buyer loyalty. Customer support points: whether or not via billing and fee of insurance policies or claims funds, can drive prospects away. Clients nonetheless, figuratively, vote with their toes.

Roundtable views on insurance coverage billing and funds

Deloitte and Majesco hosted a roundtable with skilled billing and funds business leaders to debate the market traits and subsequent methods and techniques to raise billing and funds as a key a part of the shopper journey and expertise. We documented a number of the findings and most of the roundtable discussions in a current thought management report, Rethinking Billing and Funds within the Digital Age.

In a day and age the place competitors is as stiff because it has ever been, most of our members agree that billing and funds deserve nearer scrutiny, better consideration, and better precedence in order that it reaches its full potential as an environment friendly, efficient model builder.

Stepping As much as the brand new period of buyer billing and fee expectations

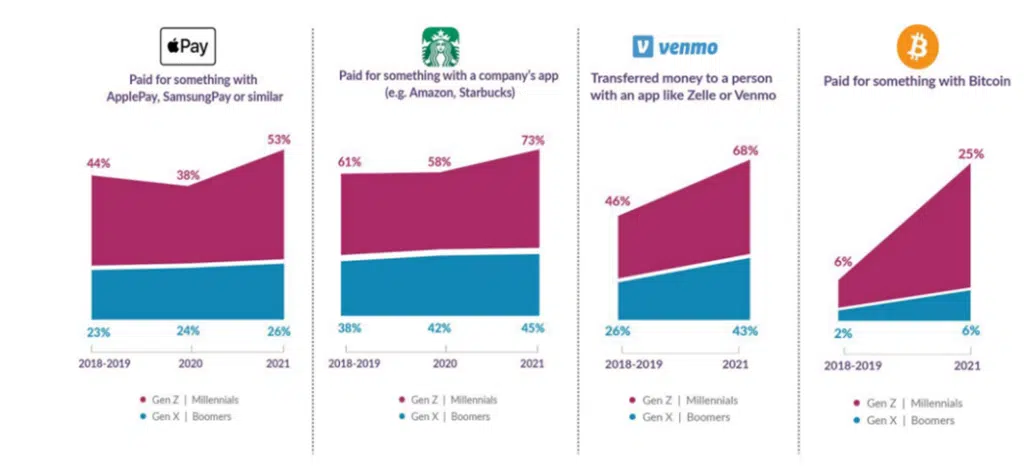

We see it throughout all industries and companies – prospects are listening to how they’re billed and paid. Their expectations, whether or not met or unmet, are one figuring out think about whether or not they select to modify to or stick with an insurer. These expectations are being pushed by an ever-growing set of choices that embody the whole lot from customizable billing schedules to digital fee strategies like ApplePay, Venmo, firm apps, and others to make or settle for funds. On the similar time, prospects predict a seamless digital expertise.

Majesco’s buyer analysis, mirrored in Determine 1, highlights the rising demand for these various fee strategies, significantly for Gen Z and Millennials.

Determine 1: New Buyer Digital Commerce Expectations

Whereas insurers should adapt their methods to be digital-centric, some prospects nonetheless choose writing a verify. As one roundtable participant mentioned, 70% of P&C funds of their line of enterprise are made by way of verify – an astounding quantity contemplating how many individuals have tailored to digital choices. To retain belief and loyalty, and hold income unobstructed, insurers should meet all billing and fee choices.

These rising expectations speed up the shift of billing and funds from its conventional position as one of the “again workplace” processes to the “entrance workplace” as an important functionality in delivering an awesome buyer expertise. Insurers more and more notice the numerous position that billing performs. They’re waking as much as the truth that distinctive service is essential past the monetary operation. First-rate service is essential to constructing and enhancing relationships with prospects, companions, and distributors. In immediately’s more and more digital world, legacy billing programs don’t meet these rising wants and expectations.

Cultivating buyer experiences that assist the model.

Superior billing and fee capabilities can not be considered merely from a transactional perspective, however now should fill an important position in creating an inviting and holistic digital expertise. Each contact level is a chance to humanize and personalize the model relationship and strengthen model belief and loyalty.

In rethinking billing and funds, insurers are targeted on key enterprise priorities together with:

- Buyer expertise – The prevalence of digital shopping for and fee choices throughout different industries, heightens the expectation for insurance coverage to ship related capabilities to be “on par.” Insurers compete with exterior experiences.

- Transparency and adaptability – Buyer belief is influenced by transparency.

- Clients are on the lookout for a single invoice for a number of insurance policies, no matter product or section.

- New merchandise reminiscent of usage-based or gig insurance coverage (which replicate actuality, not estimates) require extra frequent and personalised pricing and billing.

- Clients need to run situations. Can they preview the affect on payments if they modify plans or choices?

- Superior analytics for model administration – Insurers need perception into:

- Propensity to resume or lapse.

- Probably response charges for cross-sell or upsell gives.

- Buyer expertise satisfaction.

- And, profitability for proactive/responsive enterprise administration.

- Worth-Added Providers – More and more insurers wish to improve the shopper relationship and develop income by providing value-added providers. The billing and fee choices for these providers usually require completely different approaches than conventional threat merchandise.

Communication is vital.

Well timed, frequent, and personalised digital communication is equally as essential.

Digital channels like voice, good audio system, e mail, or textual content/SMS are more and more used to reinforce the connection and expertise. Communications are not restricted to billing statements or fee statuses. Frequent communication relating to different merchandise or value-added providers is appropriate. How are insurers changing into useful, not simply transactional? Options relating to various billing choices that may higher align with a buyer’s life might present better buyer personalization and engagement. It’s more and more essential to keep away from coverage lapses or late renewals.

“Funds, from a billing perspective, is essentially the most frequent touchpoint that you’ve got at any given level along with your insurers. That is the chance to have that nice buyer expertise, the place they are saying this was straightforward, this was frictionless.”

Roundtable Participant

Insurers should strategically and tactically start to carry billing and funds into buyer expertise and digital engagement plans. A various set of digital fee choices, superior applied sciences, and a coordinated mixture of digital communication strategies will lay a stable basis and meet the rising expectations of shoppers, brokers, and companions.

“We’ve created an organizational change administration workforce beneath our chief expertise officer. They’re constructing out a complete portfolio of messaging. We need to perceive the obstacles that folks see. If we will get that data and communicate again in phrases they’re utilizing, we will affect them to the setting we would like.”

Roundtable Participant

Digital billing and funds: the place do insurers start?

Digital billing and funds can re-energize an insurer’s potential to satisfy retail traits head-on.

To get to the subsequent degree and rethink billing, they wanted to beat hurdles like crippling legacy debt that hinders their effectiveness and buyer expertise because it pertains to billing and funds and rethink their future state. What alternatives would come up if insurers may grow to be extremely digital, with a brand new working mannequin and a stable, but versatile know-how basis?

Take care of the hurdle of legacy debt.

One of many vital hurdles for digital transformation is legacy debt – each the working mannequin and know-how – stifling an insurer’s potential to satisfy buyer digital expectations, develop billing and fee choices and drive down operational prices. An insurer’s legacy debt removes the power to launch new, revolutionary merchandise reminiscent of embedded, on-demand, UBI, and value-added providers as a result of limitations of the know-how. Billing know-how like Majesco Billing for P&C, Majesco Billing for L&AH, Majesco Digital Digital Bill360 for P&C and our ecosystem of companions allows, not inhibits.

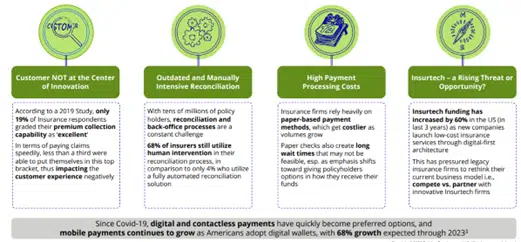

Every of the areas mirrored in Determine 2, highlights the market development challenges and operational realities of legacy debt.

Determine 2: Present state of funds within the insurance coverage sector

Addressing the present state requires a technique and plan that tackles the operational mannequin, together with all processes, know-how, and tradition. Right now’s prospects anticipate their most well-liked manufacturers to instinctively replace their processes and transaction capabilities to maintain up with what their units and existence have made attainable.

They need a threat product, value-added providers, and an expertise that gives them with what they should handle their lives. Insurers should humanize the method and expertise. However conventional product-oriented methods handicap insurers. Insurers must “suppose exterior their very own bins” and hold buyer lifecycles and wishes in focus.

Insurers that take note of these shifts ought to take the subsequent step and make fast strikes to take away their crippling legacy debt.

Unify the know-how technique and customer-focused techniques.

The longer term state calls for an operational mannequin and know-how that gives a basis to adapt, innovate and ship at pace to execute technique and market shifts. The rising significance and adoption of platform applied sciences, APIs, microservices, digital capabilities, new/non-traditional knowledge sources, and superior analytics capabilities at the moment are essential to market management.

From the entrance workplace to the again workplace, SaaS next-generation platforms are reshaping the enterprise focus from coverage to buyer, from course of to expertise, from static to dynamic pricing, from point-in-time underwriting to steady underwriting, from the historic view of information to predictive and prescriptive knowledge, from conventional merchandise to new, revolutionary merchandise, and a lot extra. Insurers’ potential to ship elevated worth to the shopper relationship will deepen and differentiate buyer loyalty.

Central to the elevated worth is bettering buyer selections, but with alternative comes complexity. This complexity could be simplified, managed, and optimized with a next-gen billing and fee unified technique.

A unified billing and fee technique offers a holistic, enterprise method to enterprise capabilities, processes, and buyer engagement. It strikes billing and funds from the again workplace and a defensive place to the entrance workplace and an offensive place for buyer engagement, resulting in greater satisfaction, loyalty, and retention.

Conventional instance: Direct and Company Invoice

Direct and Company invoice are two of essentially the most used billing sorts. Direct invoice is when an insurer sends the invoice to the policyholder for fee on to the insurer. In distinction, company invoice the company payments the insured and collects the premium then pays the insurer. Particular processing is required to assist each of those. There are different forms of billing together with checklist or group invoice, third social gathering invoice (reminiscent of mortgagees), and cut up or multipayer billing.

Whereas these proceed to be dominantly used, as merchandise change and the way premium is calculated – extra steadily or in real-time – revolutionary billing choices are rising. Insurers should be capable to assist these new choices to satisfy product calls for of shoppers.

Progressive instance: Computable contracts

One tactic of an offensive technique that’s being thought-about by some corporations is together with the power to have computable contracts (placing the coverage settlement into code) for every coverage. For instance, a rock hits your windshield. You’re taking an image and submit a declare. As a result of the information about your automobile and coverage are recognized via this computable contract, the fee can circulate instantly and digitally. The method is quick, and it naturally reduces operational prices.

Innovation targeted on the shopper can drive further offensive performs whereas accelerating transformation. Making a holistic buyer expertise not solely offers digital billing and fee choices, but additionally allows broader communication and engagement together with cross-sell or up-sell of insurance policies with further merchandise, amendments, or value-added providers primarily based on their distinctive demographics.

Progressive instance: Purchase now, pay later.

Inflation is inflicting prospects to judge all their bills. In consequence, some are contemplating various financing choices reminiscent of Purchase Now, Pay Later (BNPL). BNPL is a comparatively low-cost, versatile credit score possibility that gives sooner entry to credit score in comparison with different unsecured mortgage merchandise, thereby lowering uncertainty and easing buy choices for patrons.

This feature is primarily pushed by Fintechs who’re providing entry to credit score for patrons with low credit score scores. It offers them the merchandise they want with a decrease up-front duty. They obtain:

- Prompt gratification (not like layaways).

- Higher money circulate administration via versatile reimbursement plans & rates of interest (0-30%).

- A considerably extra non-public and secure transaction that is more cost effective and extra accessible than bank cards.

It’s estimated that 40% of shoppers anticipate installment loans as a fee possibility, however in main downturns, Deloitte estimates that installment loans can act as an essential bridge for over 90% of shoppers.

This fee possibility might be a consideration in serving to individuals pay massive premiums. For some insurers, this sort of tactic might not appear essential. Nonetheless, should you think about that a part of model constructing is making transactions straightforward and painless, it suits squarely inside the insurance coverage model technique.

In our subsequent weblog, we’ll take a look at how insurers can arrive on the future state. How can insurers select and use the best mixture of billing and fee applied sciences that may match customer-focused methods and construct the model via the absolute best experiences? Deloitte and Majesco collectively are working ahead pondering, main insurers within the business, to rethink their billing and funds operation and know-how to raise their model and buyer loyalty in a world of quickly altering expectations.

For a deeper look, remember to obtain the Majesco/Deloitte report, Rethinking Billing and Funds within the Digital Age.

Right now’s weblog is co-authored by Denise Garth, Chief Technique Officer at Majesco, and Ajay Radhakrishnan, Principal, Deloitte Consulting